Step-up in basis calculator for inherited property planning.

Model Section 1014 step-up in basis scenarios so accountants can explain inherited-property gain, FMV basis resets, and tax savings more clearly.

Built for CPA firms helping families and real-estate clients think through inherited property decisions.

Tax advisors, estate-planning accountants, and real-estate CPAs working on inherited property scenarios.

Use it when a client inherits property, needs to understand stepped-up basis, or wants to compare a prompt sale with a later disposition.

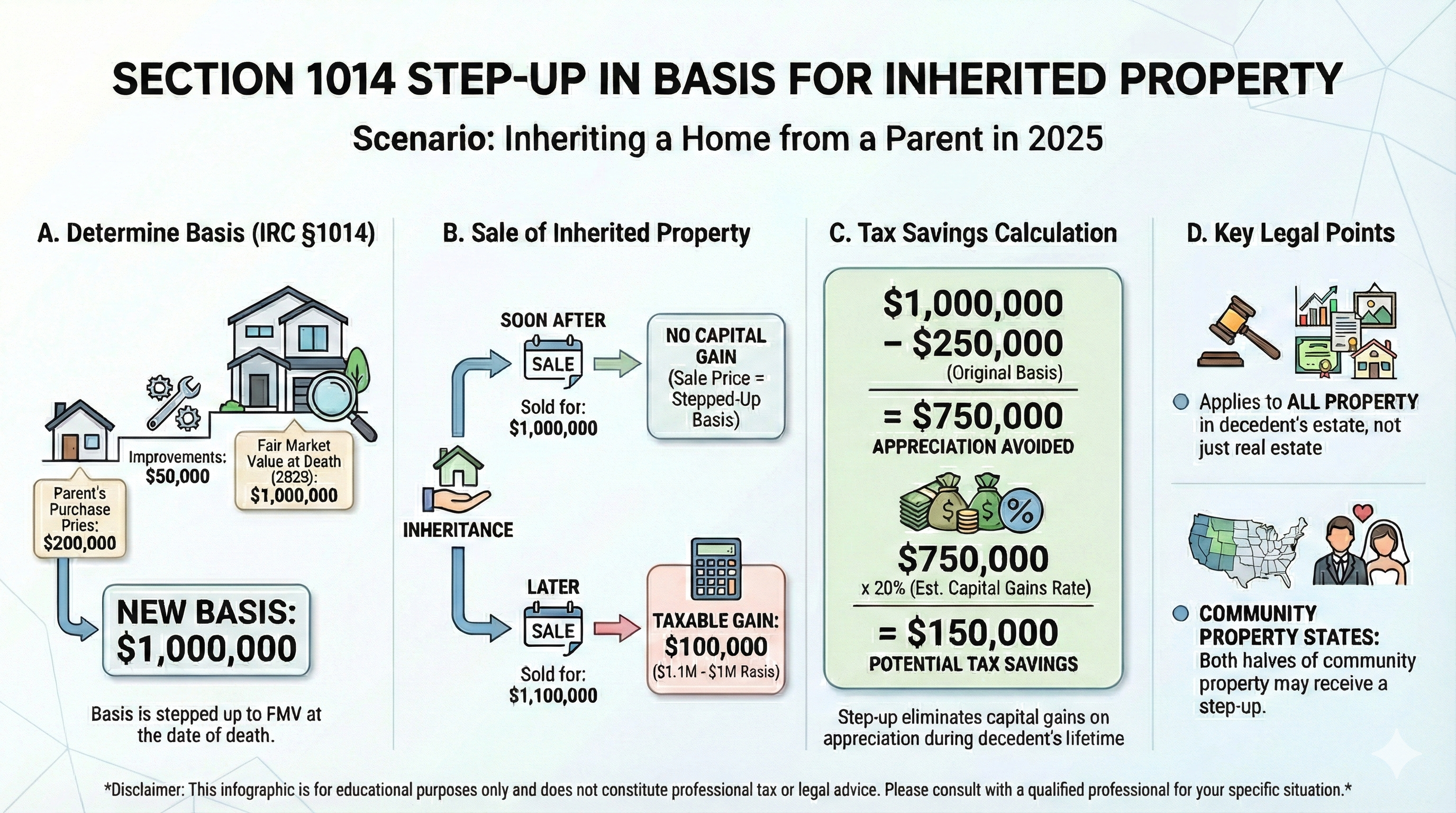

The page helps firms explain how fair market value at death resets basis and changes the taxable gain picture.

A clearer way to move from client inputs to planning outputs.

The page mirrors how firms think through the work: what goes in, what comes out, and what the client needs help understanding.

An heir needs to know whether selling inherited property soon changes the tax outcome.

The accountant can compare original basis to stepped-up basis, show the appreciation that disappears at death, and explain how later appreciation would still be taxed on a future sale.

Open in workspaceTranslate Section 1014 into plain client language.

Show basis reset and gain avoidance in one screen.

Frame inherited-property decisions without spreadsheet sprawl.

Questions firms ask before using this calculator.

Is this only for real estate?

The concept applies more broadly, but this page is especially useful for real-estate and inherited-property planning conversations handled by CPA firms.

Can the calculator replace estate administration advice?

No. It supports tax modeling and explanation, while legal, estate, and filing details still need professional review.

Why is the fair market value date important?

Because the stepped-up basis usually hinges on the value at death, and that value drives how much appreciation is removed from future gain calculations.

Keep the topical path connected.

These pages are built to help firms move across related planning questions without dropping back into disconnected spreadsheets.